Learning objectives

- Define and describe the properties of autoregressive (AR) processes.

- Define and describe the properties of moving average (MA) processes.

- Explain how a lag operator works.

library(tidyverse)

## -- Attaching packages --------------------------------------------------------------------------------- tidyverse 1.3.0 --

## v ggplot2 3.3.2 v purrr 0.3.4

## v tibble 3.0.3 v dplyr 1.0.2

## v tidyr 1.1.2 v stringr 1.4.0

## v readr 1.3.1 v forcats 0.5.0

## -- Conflicts ------------------------------------------------------------------------------------ tidyverse_conflicts() --

## x dplyr::filter() masks stats::filter()

## x dplyr::lag() masks stats::lag()

set.seed(25)

MA_mean = 2.0

MA_weight = 0.5

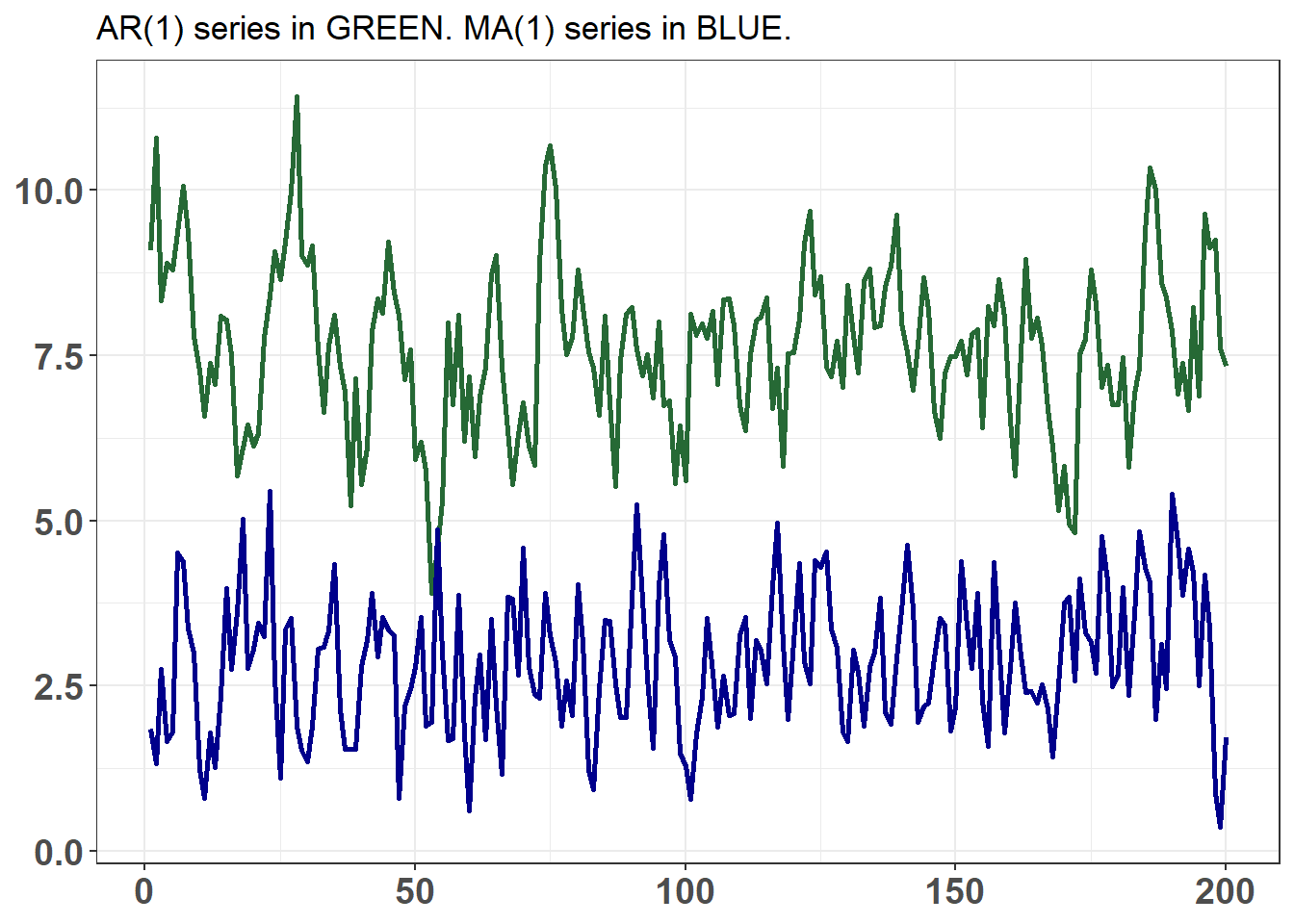

# Generate an MA(1) with mean, μ = 2.0 and weight parameter 𝜃= 0.5

MA <- arima.sim(model=list(order = c(0,0,1), ma = MA_weight), n = 200, mean = MA_mean)

AR_intercept = 3.0

AR_param = 0.6

# Generate an AR(1) with intercept δ = 3.0 and AR parameter ϕ = 0.6

AR <- arima.sim(model=list(order=c(1,0,0), ar = AR_param), n = 200, mean = AR_intercept)

color_AR = "#266935"

color_MA = "darkblue"

time_ma_ar <- bind_cols(MA, AR) %>% rowid_to_column() %>%

rename(y_MA = ...1, y_AR = ...2)

## New names:

## * NA -> ...1

## * NA -> ...2

time_ma_ar %>% ggplot(aes(x = rowid)) +

theme_bw() +

theme(

axis.title.y = element_blank(),

axis.title.x = element_blank(),

axis.text = element_text(size = 14, face = "bold"),

legend.position = c(0.8, 0.86)

) +

ggtitle("AR(1) series in GREEN. MA(1) series in BLUE.") +

geom_line(aes(y = y_AR), color = color_AR, size = 1) +

geom_line(aes(y = y_MA), color = color_MA, size = 1) +

scale_y_continuous(breaks = c(0, 2.5, 5.0, 7.5, 10, 12.5))

# scale_color_manual(name = "Simulations with arima.sim()", labels=c("MA(1)", "AR(1)"))

# MA mean is intercept

lr_mean_AR <- AR_intercept/(1 - AR_param)

variance_MA <- (1 + MA_weight^2)*1

variance_AR <- 1/(1 - AR_param^2)

lr_mean_AR

## [1] 7.5

variance_MA

## [1] 1.25

variance_AR

## [1] 1.5625