BT Question Set P1-T2-21-1: Non-stationary time series

21.1.1 This is a seasonal model without a trend

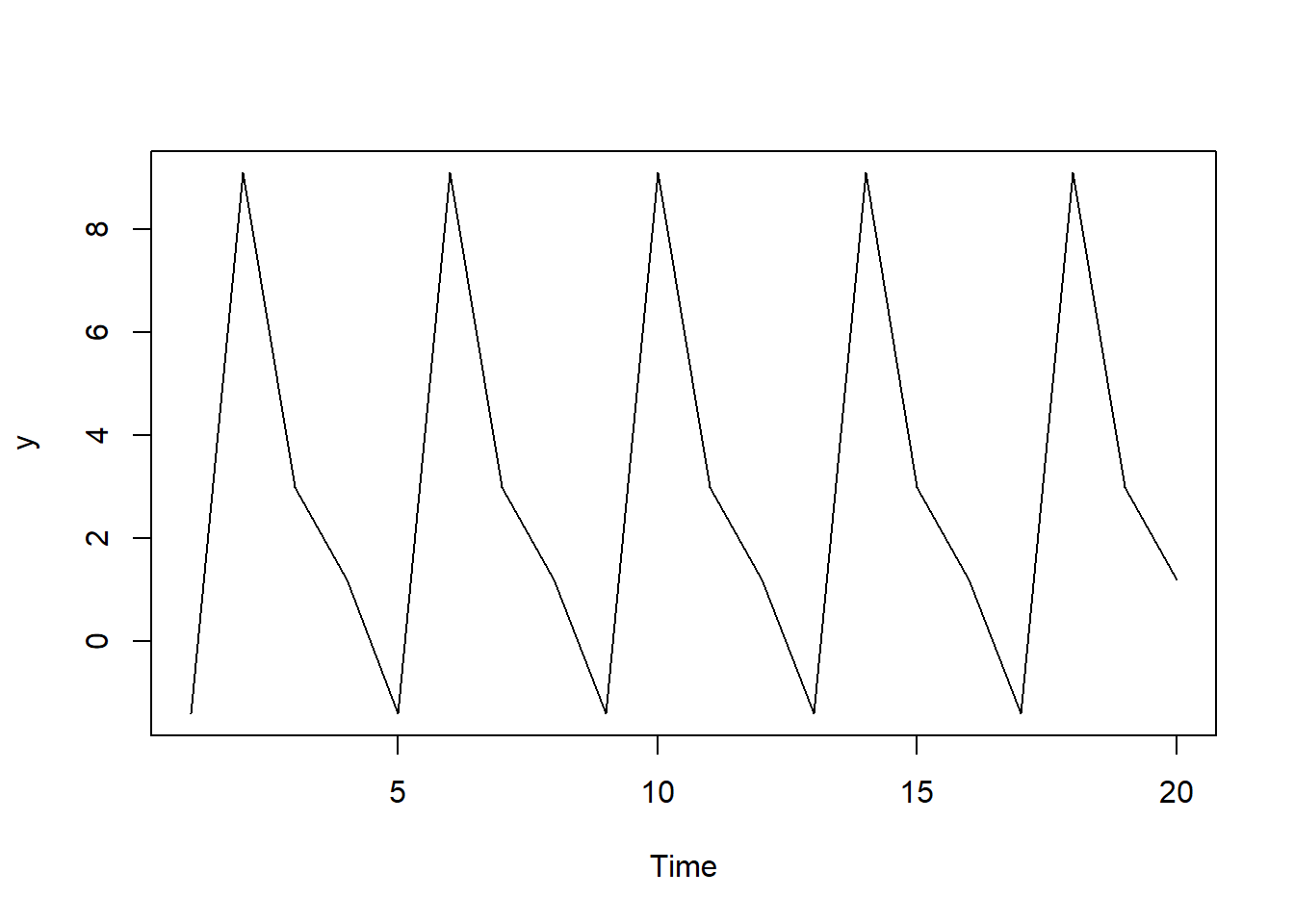

21.1.1 The following seasonal dummy model estimates the quarterly growth rate (in percentage terms) of housing starts … The model’s intercept (δ) equals +1.20 and the gamma coefficients are the following: γ(1) = -2.60, γ(2) = +7.90, and γ(3) = +1.80. According to this model, when does the growth rate peak?

# similar to GARP's EOC 11.8, there is no trend, only seasonality

c_delta <- 1.20; gamma <- c(-2.6, 7.9, 1.80, 0)

quarters <- rep(1:4, 5)

y = c_delta + gamma[quarters]

ts.plot(y)

21.1.2 An AR(2) that is stationary as demonstrated by |roots| > 1.0 but also our ability to simulate

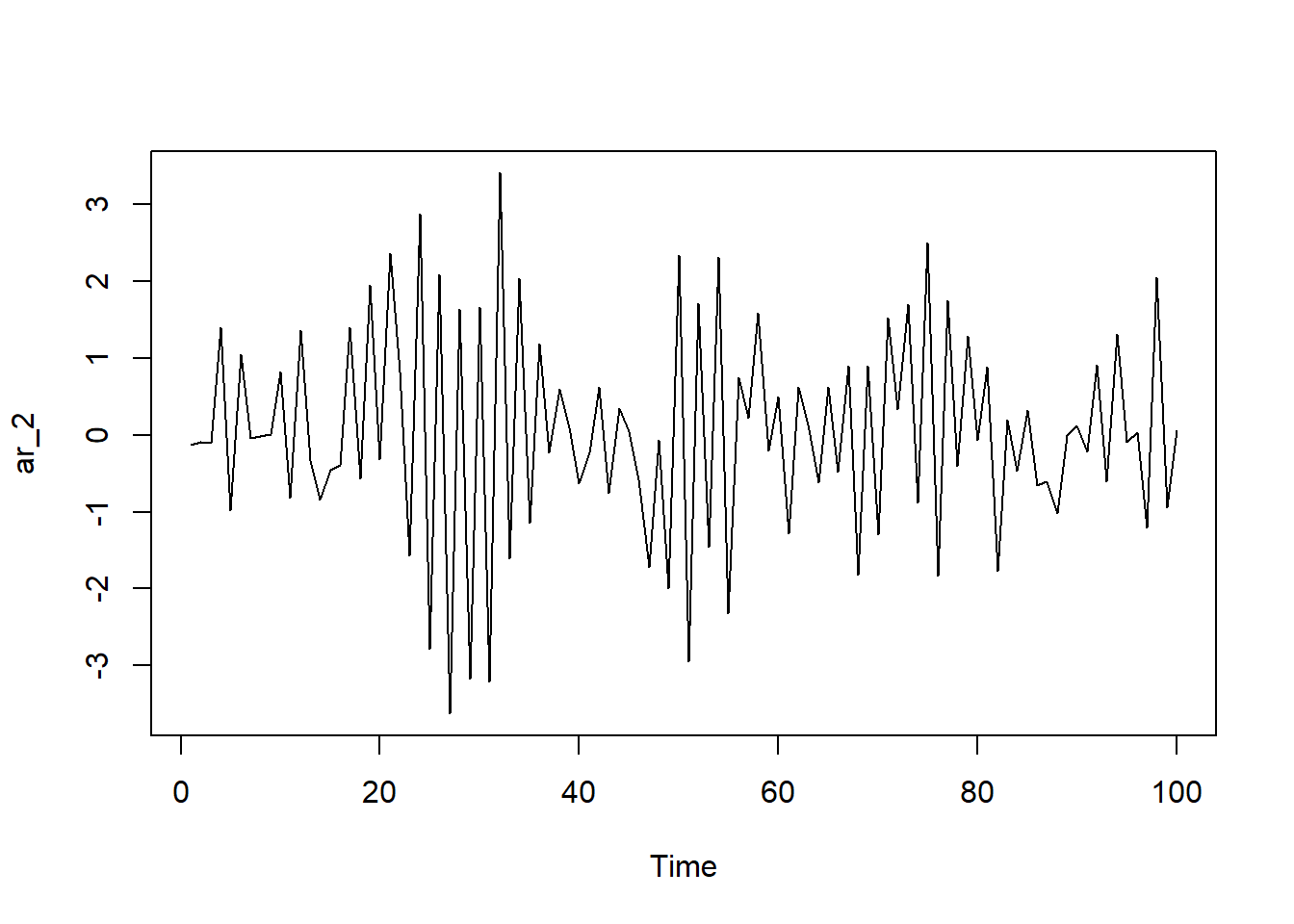

21.1.2. Peter wants to model the following AR(2) time series: Y(t) = 0.750Y(t-1) - 0.1250T(t-2) + e(t). He wonders if this AR(2) is stationary. He realizes that he can write this as a log polynomial …

# install.packages("polynom", repos = "http://cran.us.r-project.org")

library(polynom)

peters_poly <- polynomial(coef = c(1, -0.75, 0.125))

peters_poly## 1 - 0.75*x + 0.125*x^2solve(peters_poly) # the roots (aka, zeros) are 2 and 4## [1] 2 4ar_2 <- arima.sim(model=list(order=c(2,0,0),ar = c(-0.75, 0.125)),n = 100)

ts.plot(ar_2)

21.1.3 Compares a deterministic trend to a stochastic (random walk with drift) trend

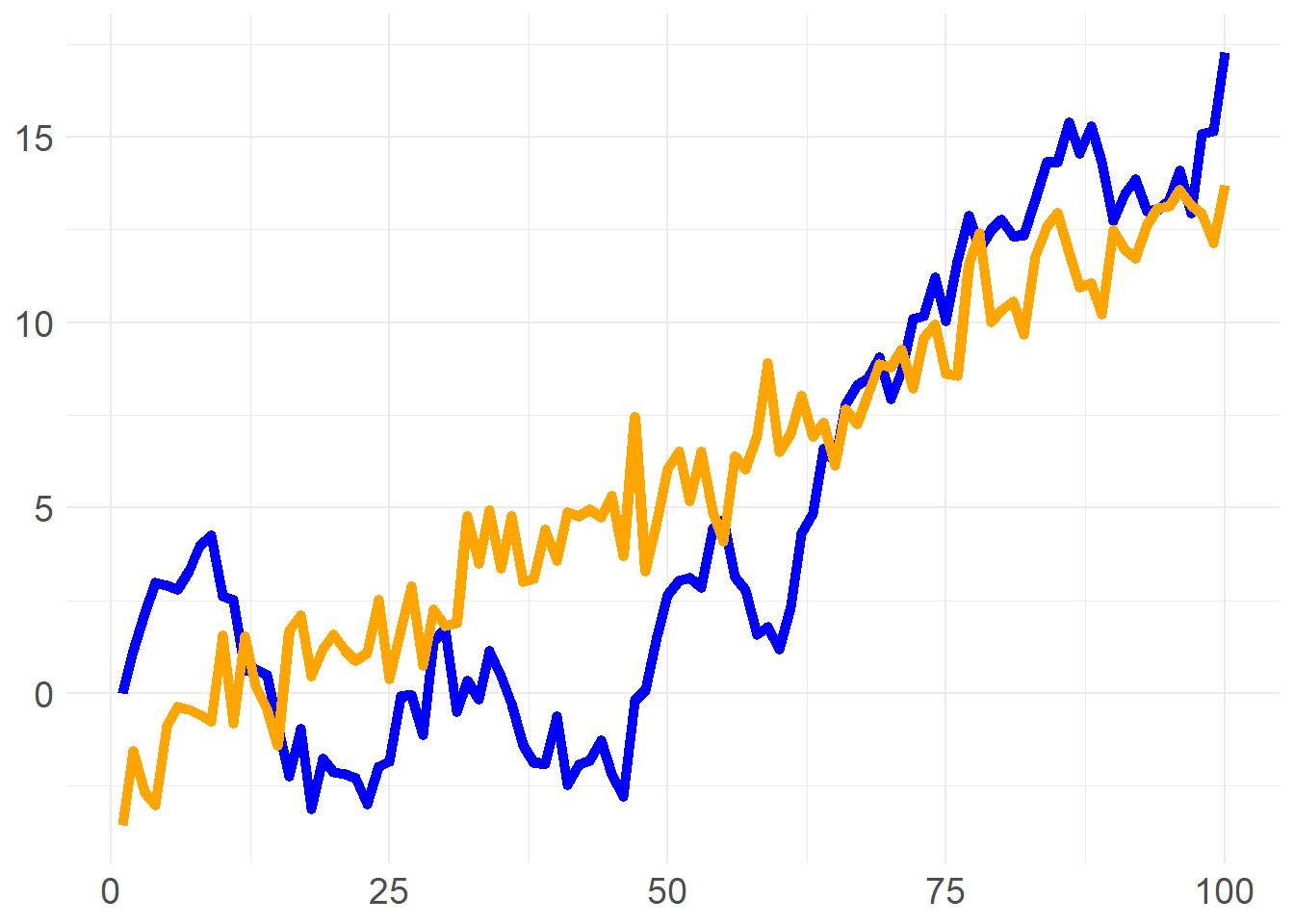

21.1.3. Sally considers two series for her model: a linear trend model (aka, deterministic trend), and a random walk with drift. Each is simulated below (n = 100 steps)

library(tidyverse)## -- Attaching packages --------------------------------------------------------------------------------- tidyverse 1.3.0 --## v ggplot2 3.3.2 v purrr 0.3.4

## v tibble 3.0.3 v dplyr 1.0.2

## v tidyr 1.1.2 v stringr 1.4.0

## v readr 1.3.1 v forcats 0.5.0## -- Conflicts ------------------------------------------------------------------------------------ tidyverse_conflicts() --

## x dplyr::filter() masks stats::filter()

## x dplyr::lag() masks stats::lag()library(ggthemes)

library(RColorBrewer)

set.seed(28)

n <- 100

x <- 1:n

# white noise

white_noise <- arima.sim(model = list(order = c(0,0,0)), n = 100)

#linear trend

linear_tr <- -1.8 + 0.15*x

time_trend <- linear_tr + white_noise

rw_drift <- arima.sim(model = list(order = c(0,1,0)), n = n-1, mean = 0.4)

trends <- data.frame(

x,

time_trend,

rw_drift

)

p1 <- trends %>% ggplot(aes(x=x)) +

geom_line(aes(y=rw_drift), color = "blue", size = 2) +

geom_line(aes(y=time_trend), color = "orange", size = 2) +

theme_minimal() +

theme(

axis.title = element_blank(),

axis.text = element_text(size = 14)

)

p1## Don't know how to automatically pick scale for object of type ts. Defaulting to continuous.